NEW YORK (CNNMoney.com) -- Most analysts see the Fed cutting rates for the third consecutive time tomorrow. What investors don't know is just how deep the Fed will cut. What will this mean for your mortgage? Here's what you need to know.

NEW YORK (CNNMoney.com) -- Most analysts see the Fed cutting rates for the third consecutive time tomorrow. What investors don't know is just how deep the Fed will cut. What will this mean for your mortgage? Here's what you need to know.1: Long-term mortgages won't move much

Right now investors are split on whether the Fed will lower the funds rate by another quarter point to 4.25% or cut it by a half-point, to 4%. But the fact is, there's not much doubt that the Fed will cut rates. And because of that, the market has already priced that in, says Mike Larson with moneyandmarkets.com. 30-year fixed rates have been falling for some time.

In July, the average rate on a 30-year fixed mortgage was 6.66%. Last week, it was 5.82%. So, a rate cut won't really do very much to lower long-term rates. They're already low. So if you want to refinance, it's a good time to start shopping.

2: ARM resets not as severe

The Fed move tomorrow may be more significant to borrowers with adjustable-rate mortgages than what the government is doing in freezing subprime interest rates. That's according to Greg McBride at bankrate.com. Most resets on adjustable rate mortgages will reset in the middle of next year. And the fact that the Fed is cutting rates, will make these resets more manageable for prime borrowers, which aren't covered by the foreclosure-prevention plan announced last week.

So, if you had an adjustable rate mortgage that started at 4.5% and your rate was going to reset at 7.5%, you may only face a rate reset of 5.7%.

3: HELOCS will be cheaper

Home equity lines of credit will be cheaper if the Fed does cut rates. It may take up to three billing cycles to see the actual decrease in your bill. If you need to consolidate debts or you need money for medical bills or college expenses, you may consider shopping around for a HELOC since lenders are likely to price in the Fed's cut immediately.

4: Keep it in perspective

The take away here is that the Fed is on your side. This rate cut won't be the silver bullet that fixes the housing market. But it's apparent that Fed is in a rate cutting mode, and the cumulative effect on that will help consumers. There are a number of things the Federal Reserve can't control, like the impact of the credit crunch.

You need to look at inflation, job growth and the overall health of the economy as indicators of when this housing crisis may subside. When we get down to it, there are two issues here, according to McBride. That's inventory of houses on the market and the affordability of buying a home. Interest rate cuts won't do much to make that go away. Sometimes, it's just a matter of time.

Money, Money, Money

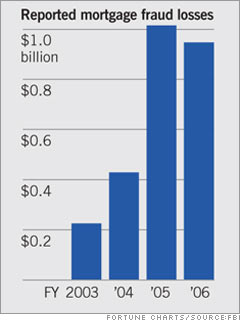

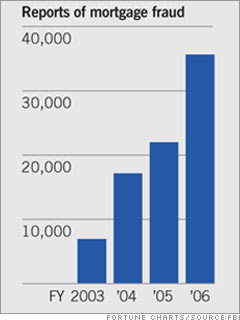

A con artist looks for a low-end, rundown house for sale. He approaches the seller and says he's willing to pay the full asking price-but only if the seller will do him a small favor. See, the buyer needs a bigger mortgage than the house is worth. So if the owner agrees to relist the house at, say, triple the price, then the buyer can apply for a bigger mortgage.

A con artist looks for a low-end, rundown house for sale. He approaches the seller and says he's willing to pay the full asking price-but only if the seller will do him a small favor. See, the buyer needs a bigger mortgage than the house is worth. So if the owner agrees to relist the house at, say, triple the price, then the buyer can apply for a bigger mortgage. Con artists use a "straw man" or "straw buyer" to purchase a property. A straw buyer is usually someone fairly unsophisticated who has passable credit. Often straw buyers are told by the huckster-a mastermind who uses a false identity and typically poses as a sophisticated investor-that they'll get a nice chunk of money if they go in on a plain-vanilla business transaction with him.The straw buyer gets a mortgage on

Con artists use a "straw man" or "straw buyer" to purchase a property. A straw buyer is usually someone fairly unsophisticated who has passable credit. Often straw buyers are told by the huckster-a mastermind who uses a false identity and typically poses as a sophisticated investor-that they'll get a nice chunk of money if they go in on a plain-vanilla business transaction with him.The straw buyer gets a mortgage on

NEW YORK (CNNMoney.com) -- A senate panel is scrutinizing the fees and billing practices of the credit card industry. The good news is that reform may be on the way. But we'll give you the tools you need to protect yourself now from credit card fees.

NEW YORK (CNNMoney.com) -- A senate panel is scrutinizing the fees and billing practices of the credit card industry. The good news is that reform may be on the way. But we'll give you the tools you need to protect yourself now from credit card fees. 1. Make sure you are getting the right vehicle.

1. Make sure you are getting the right vehicle. ized. Home purchases are assets that will probably increase in value, and debt used to purchase homes is "good" debt, or at least "not as bad as bad debt." Good debt is typically less expensive than bad debt--mortgage interest rates typically are much lower than credit card interest rates, for instance. Mortgage payments also are typically tax deductible, while the interest on credit cards and similar loans are not.

ized. Home purchases are assets that will probably increase in value, and debt used to purchase homes is "good" debt, or at least "not as bad as bad debt." Good debt is typically less expensive than bad debt--mortgage interest rates typically are much lower than credit card interest rates, for instance. Mortgage payments also are typically tax deductible, while the interest on credit cards and similar loans are not.